In our previous blog post, Geodata for Financial Institutions Part 1, we discussed the difficulty of developing geodata based products and services for new markets that are not necessarily familiar with geodata. We found Financial Institutions (FI) to be an interesting new market for geodata. This blog shows how Satelligence developed a deforestation risk product that is aligned with FI workflows and already used in engaging investees.

Types of Financial Institutions

For this blog, we focus on two types of Financial Institutions:

Investment Funds raise capital from Asset Managers and other institutional investors (e.g. pension funds and insurance companies) to directly invest (through active, private ownership) in agriculture or forestry companies across the value chain.

Asset Managers raise capital from other institutional (e.g. pension funds and insurance companies) and retail investors (private individuals) to indirectly invest (through public ownership or lending) in agriculture or forestry companies across the value chain.

Financial Institutions, what makes them tick?

To develop a new product for a new market you have to understand the pains and gains of the market, in this case the FI market. What hurts them (pains), like negative publicity from being linked to illegal deforestation, and how money is made (gains), like Return On Investment.

The pains of the FI market are very similar to the pains of the stakeholders in the commodity value chain, consisting of producers, traders, manufacturers and retailers; commodity production linked to illegal deforestation is causing bad PR, loss of important clients and loss of private or public (stock market) value .

But the gains are very different. While stakeholders in a commodity value chain make money directly by handling and selling the commodity in whichever processed form, Financial Institutions make money by profitable handling of money: they invest capital. Asset Managers typically collect cash from different sources (e.g. pension funds, insurance companies and private individuals) and allocate it to different investment categories:

Bonds, equities, alternative investments

Zooming in on bonds, the worldwide GDP growth is in a downward trend, most likely to continue for the foreseeable future. There is a strong correlation between GDP growth and the returns on government bonds. Hence, it becomes more and more difficult to make money out of bonds.

Therefore, the push to the other two categories, equities and alternative investments, will continue in the mid- to long-term.

If we look at equities, we have seen strong recent peaks in the valuation of listed shares in the last few years. Given that listed shares have become relatively expensive and the worldwide economic outlook is grim, the expected return going forward is (relatively) low. That leaves alternative investments as the most promising option.

Alternative investments are basically an investment in any asset class excluding stocks, bonds, and cash. One of these alternative investments is Agriculture & Forestry with typical annual nominal returns between 6 to 10% (depending on the geography) over the last two decades. Institutional and retail investors are very keen to invest in these assets given the tangible nature, relatively fixed long-term cash flows (from selling crops or timber) and the sustainability angles (e.g. carbon credits). The challenges with these kinds of investments is that they are illiquid (i.e. more difficult to sell quickly compared to e.g. stocks) and only pay off after a certain period (for example a crop has to grow to full maturity before it can be harvested).

What is happening with our investments?

Because of the tangible and long-term profile, Financial Institutions would like to keep track real-time of what is happening with their investments. Such information is not only key for internal (risk) performance evaluation but also external reporting to its clients (institutional and retail investors) on important themes such as deforestation.

Investment Funds have a much more narrowed investment strategy by focussing only on one or a few alternative investment asset classes, such as agriculture and forestry. For internal (risk) performance monitoring and external reporting to clients, real time tracking information on specific themes is key.

In particular, we see a high interest of Investment Funds for specific themes such as land use & restoration, deforestation and carbon (with a total market size of € 35b. Asset managers are mainly interested in the themes of biodiversity, deforestation, carbon and water (with a total market size of € 45b.

From maps to reports

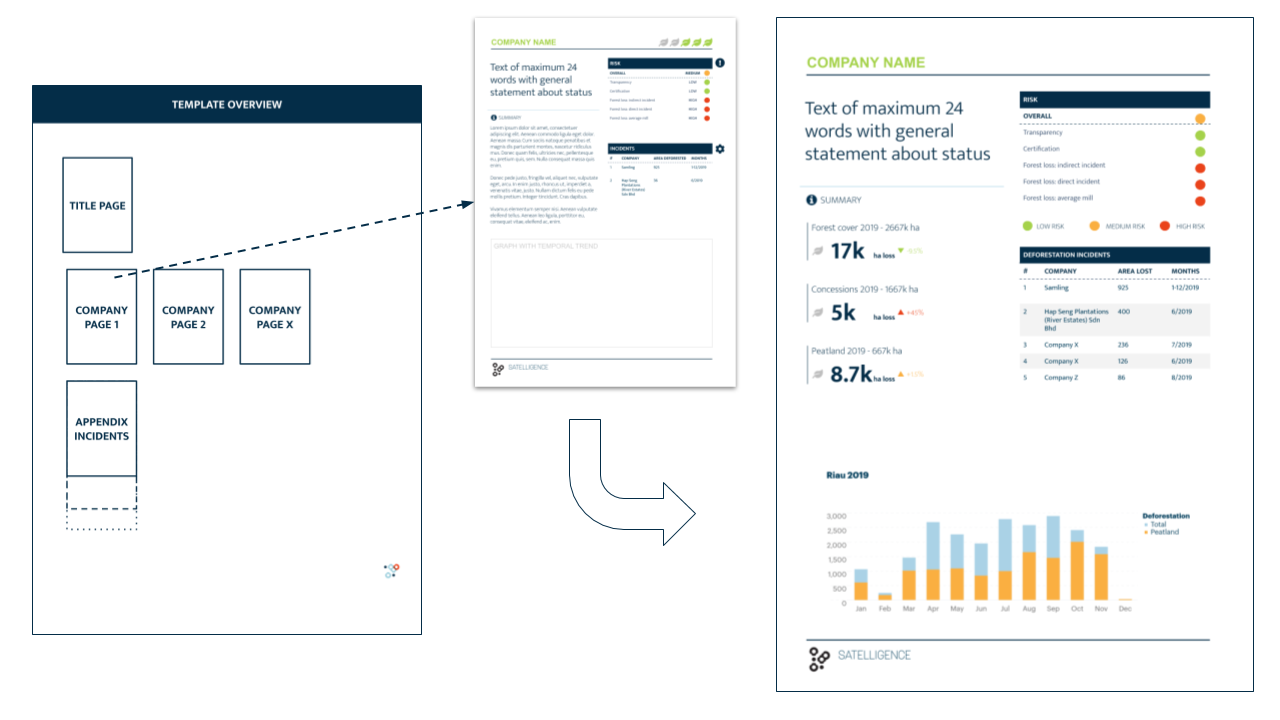

Combining these insights (risk insights in portfolios as well as monitoring assets) with what we do at Satelligence led to the development of concept risk reports that iterated into actionable deforestation risk reports. The data in these reports are exactly the same as the data we present in our online app for supply chain stakeholders. But the perspective (companies) and the way it is presented is different.

The figure below shows an example of one of the iterations of the report. The report is not only based on how we fit our data and technology to the users problem, but also focuses on what and how the user is going to use this report in day to day work; these reports are for example used in bi-weekly portfolio management meetings where companies are screened for risk of being linked to deforestation. If needed, action can be taken to engage such companies and confront them with evidence of illegal deforestation.

Conclusion

By listening to the end user and understanding their context we found that we should build a product that aligns with a financial investment portfolio, of which companies are the building blocks rather than starting from pixels, maps and satellites. Focusing on the whole story, rather than finding a problem to a solution or even stopping at fitting a solution to a problem was key in this process.

Epilogue

The trend of Financial Institutions moving their focus towards sustainable development is not new. And the first initiatives of using alternative data (amongst which geodata) are popping up as well. Those are great trends. At Satelligence we believe an economically sustainable business is an environmentally sustainable business. But we still note a gap between the problem of the market and the solutions service providers offer.

There are two reasons for that gap:

- Solutions are often ‘tools for consultants’ or platforms for data scientists or developers;

- The data sources are either outdated, lacking in quality or not-relevant.

At Satelligence we overcome the ‘building tools & platforms’ flaw by focussing from the very beginning on the workflow and context of the customer: what is the problem and what solution fits best? And then take that one step further: what is the user going to do with our solution? What action will he/she take to get the world one step closer to zero deforestation? If that question cannot be immediately answered, the product is not yet finished.

From satellites to impact

We overcome the low quality data by providing first-rate, up-to-date, and relevant information by connecting what happens on the ground (commodity production, illegal deforestation) directly to supply chain models. Our multi-sensor change detection algorithm ensures the highest quality data, all the time, anywhere it matters. Processing that data into products that the user understands and, more importantly, uses in their day to day work is key to why our services not only look cool, but are really impactful.

Concluding, with the tailored reporting for Financial Institutions, we developed a product that fits their jargon, world view and day-to-day work. We did that by translating geospatial information into a form that they understand, is easy to read and is actionable.

#

Next article

New applications of GNSS

Global Navigation Satellite System (GNSS) technology is an enabler for numerous applications which make our lives more convenient and efficient. With the worldwide spread of the COVID19 virus, GNSS even further proves to be an invaluable technology. The struggle to tame the pandemic motivated the development of various initiatives, the feasibility of which rely on the ability to obtain accurate positioning information.

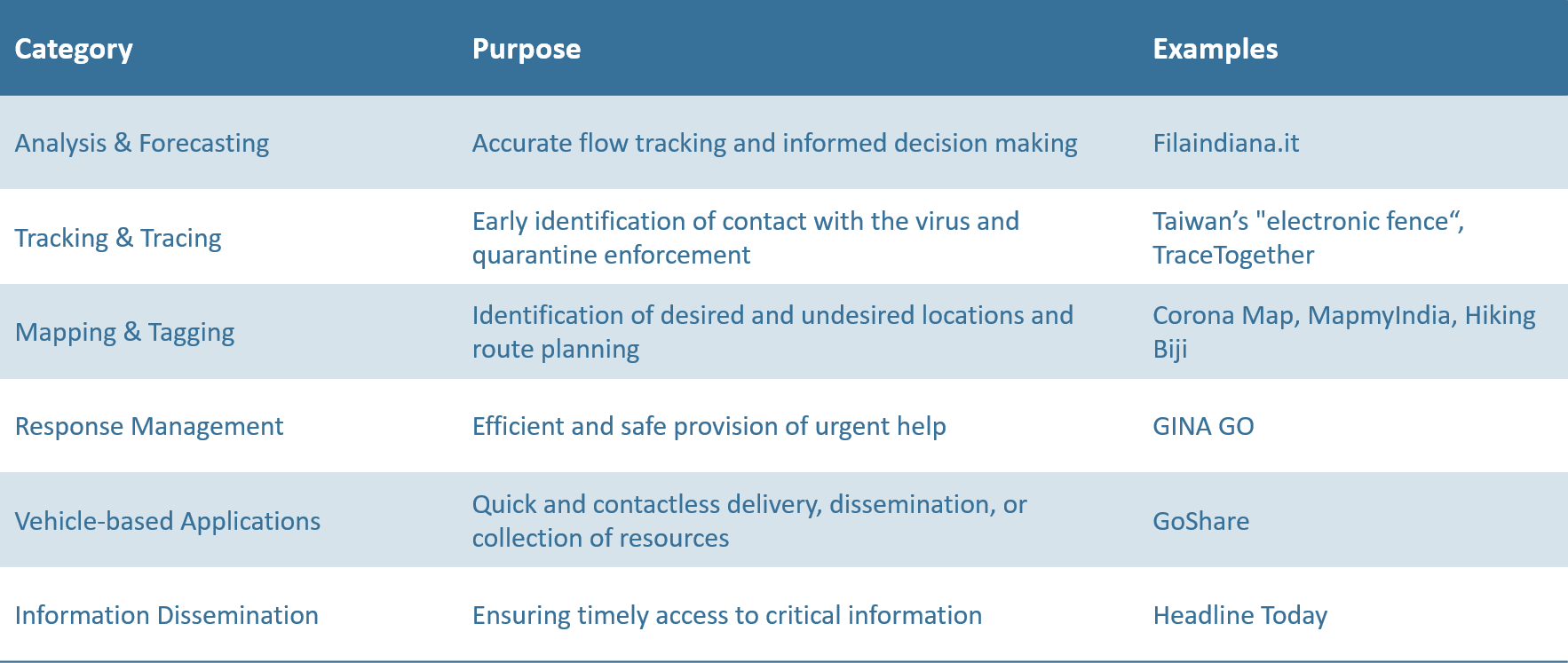

Analysis & Forecasting

Analysis & Forecasting

Thousands of GNSS terminals installed in vehicles allow increasing the efficiency of the entire road transportation system. At the level of users, location-based technology informs drivers about possible congestions and helps to optimise their route, whereas governments can leverage this knowledge to better allocate much-needed resources. In China alone, epidemic prevention and transportation service information has been sent to over 6 million vehicles, to optimise the delivery of emergency and medical materials to isolation hospitals.

Besides, tech giants such as Google or Bytedance as well as big mobile operators have a vast collection of location data on billions of their customers. Such aggregated information can be used on a small and large scale. Applications like Italy’s Filaindiana.it allow receiving near real-time updates on whether certain places like shops are currently busy or relatively empty. These insights are critical for people’s decision making regarding everyday activities, for example, when and where to go to do groceries while maintaining their physical distance from others.

At the same time, these metadata are a great resource for governments to create models of the spread of the disease for informed decision making. Such analytics can serve as a basis for forecasts as well as for the evaluation of current and potential new policies. In Germany, for instance, the government’s public-health agency Robert Koch Institute has already established such cooperation with Deutsche Telekom.

Tracking & Tracing

Tracking & Tracing

GNSS also enables the establishment and use of geofencing – location-tracking to ensure that people who are quarantined stay in their homes. If people leave the quarantine areas, as indicated by the location of their phones, they receive a warning while local authorities get notified of the defiance. To prevent people from tricking the system by leaving their gadgets at home, regular phone check-ups take place. The use of this approach in Taiwan with the help of “electronic fence” app, for instance, allowed to keep the number of infection cases incredibly low despite its proximity to China.

Detection of close contact to COVID-cases is also available now in the form of an app. In South Korea, the Now & Here application by ITL provides detailed information on local neighbourhoods, ranging from restaurants and shops to tourist attractions. The app has added COVID information to its offer, based on the user’s current location, showing where confirmed patients have passed by recently. Another prominent app is TraceTogether from Singapore. The application does not actively use GNSS/LBS, but employs Bluetooth to record contact history for subsequent encryption and storage. The record update takes place if two users of the application happen to spend over thirty minutes within two meters of each other. If one of the people ultimately gets diagnosed with the disease, the other one gets notified of this fact and also gets encouraged to undergo testing.

Mapping & Tagging

Mapping & Tagging

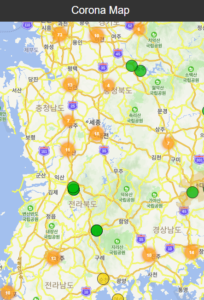

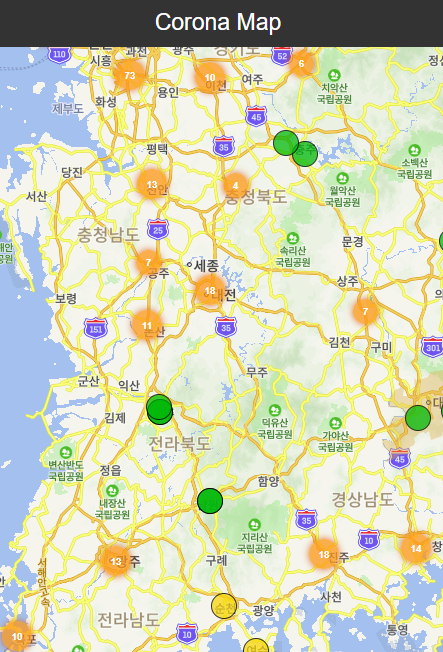

Some platforms like Corona Map in Korea are being used for tagging of dangerous areas and COVID hotspots. In other words, a map marks sites which were visited by confirmed patients and colour-codes how long ago those visits took place. This gives a much better understanding of which areas are relatively safe and which locations should better be avoided. China’s HaiGe Smart Epidemic Prevention Management Platform takes it even further by analysing the patterns of the virus spread to calculate and suggest the safest possible commuting route to the people who are not able to work from home.

Alternatively, there are apps like MapmyIndia that can be used to locate and reach the nearest specialised facility, be it a Coronavirus testing lab, an isolation centre, or a hospital. This same concept is also applied to more day-to-day locations such as an open shop or a pharmacy with available medical masks as is the case with Taiwan’s Pharmacy Locator app (Zhao Yao Ju), which is extremely useful as the island has rationed masks for its population. Needless to say, millions of people have benefited from such helpful guidance already.

Also, with gyms becoming a less and less viable option for doing sports amid the epidemic, people are starting to look for alternatives. This normally entails trying to avoid the crowds by exercising closer to nature. Currently, hiking is becoming one of the increasingly popular alternatives subsequently boosting the demand for trail map apps like Hiking Biji.

Response Management

Response Management

Another category of solutions improves the quality, speed, and safety of providing critical response services. GINA GO, for instance, is a Czech app aimed at civil servants, such as police officers, hygienic workers, firefighters, and rescuers as well as volunteers in the field. The application has a wide functionality ranging from notifying the staff of potentially dangerous zones to helping monitor infected patients and, if necessary, report an emergency situation.

Governments also use GNSS technology for a rapid expansion of infrastructure capacity in response to the skyrocketed needs. For example, the unprecedented construction of two hospitals in Hubei (2600+ beds in total) in the span of ten days would not have been possible without the GNSS-based surveying of the site.

Vehicle-based Applications

Vehicle-based Applications

Unmanned aerial vehicles (UAV), which were previously mostly used in agriculture for spraying pesticides, are now being repurposed for large-scale disinfection. With the help of precise navigation, pilots can cover areas of up to five thousand square meters within ten to fifteen minutes. This results in a fifty times higher speed efficiency as well as greatly reduces the workers’ exposure to the virus and chemicals. Another way that GNSS-enabled drones are saving lives is through fast and accurate deliveries between the areas with the Coronavirus outbreak and medical centres. Such an approach, for example, sped up the delivery of medical test samples by fifty per cent while simultaneously minimising direct human contact. Drones are also being geared with all the necessary equipment like loudspeakers and thermal sensors to effectively enforce quarantines. Each UAV is capable of patrolling an area of up to ten square kilometres which amounts to the work of one hundred police officers.

Similar concepts have been executed with the help of autonomous road vehicles. Those are being used to deliver essentials like food and medicines to people in need, as well as for disinfecting hospitals. When it comes to a smaller form factor, GNSS-powered autonomous robots complete multiple critical tasks ranging from meal deliveries to quarantined areas to performing diagnosis and conducting thermal imaging of the hospitalised.

A less novel yet still very useful GNSS application area are the individual transport sharing services. A great example of this are dockless e-scooters which can be rented with the help of an app like GoShare. The real power of such transport mode is that it allows citizens not to rely as much on public transport and therefore minimise physical contact with others.

Information Dissemination

Information Dissemination

Certain applications have been developed to ensure the delivery of important information to the population. This way, even while isolated, people have an opportunity to get their hands on the most critical information. Headline Today in China, for example, not only shares the latest updates regarding virus-related statistics or the latest government policies and directives but also enables its users to conduct a preliminary self-diagnoses by going through a symptoms-checking questionnaire.

Different approaches to a shared objective: Fighting COVID19

When looking at how different countries are fighting COVID19, there a lot of similarities in their approaches. Throughout Asia, private and public entities have used GNSS-based and other applications to inform their population, to identify nearby hospitals or pharmacies, to enforce quarantines or to trace close contacts to confirmed COVID-patients. Yet, some differences can be discerned between the diversity of approaches.

China, for instance, has taken bold and comprehensive measures to tame the pandemic. This includes mandatory applications for contact tracing, and the sharing of one’s health status using a QR-code. Compared to this approach, Japan is on a completely opposite side of the spectrum with a very strong tradition of personal privacy protection similar to the EU’s GDPR regulation. Therefore, while the tracking technology exists in Japan, location-based applications are unlikely to be used on a large scale for contact tracing or quarantine enforcement, unless there an update in legislation.

Other players fall somewhere in between the two examples from above. Both Taiwan and South Korea use GNSS-based geofencing for quarantine enforcement, and South Korea’s contact tracing teams are assisted by GNSS-driven technologies to speed up the process. It is also worth mentioning the specific situation of South Korea in regards to national technological use. The country has a near hundred per cent smartphone penetration rate, a particularly high ratio of credit and debit card use, as well as tight mobile network – both LTE and 5G. Such conditions, make Korea an excellent environment for the adoption of GNSS-based solutions against COVID19. Amongst others, these dimensions will influence whether other countries could or would replicate Korea’s policies and innovations.

Singapore, from its side, interestingly decided to opt for Bluetooth rather than location data in its TraceTogether app. The application reportedly encrypts all collected data and dispatches it only upon the request from national health authorities.

Lastly, it is noteworthy to see how India is employing a bottom-up approach by stimulating the population to contribute to the fight against the virus. For instance, the government has initiated COVID 19 Solution Challenge to crowdsource the ideas for potential products capable of taming the pandemic or at least mitigating its negative effects. India’s recently launched Aarogya Setu-application will combine location data and Bluetooth for contact tracing but also notify its users when a confirmed COVID19-patient is closeby.

European challenges and solutions

European challenges and solutions

Asia was the first continent to be hit by COVID19. Thousands of people got infected and many lives have sadly been lost before the invisible enemy could be understood and mitigated. Now, stakeholders in Europe can analyse the invaluable experiences from their Asian counterparts.

However, European countries do have a different tradition and legal context, for instance with regards to the protection of one’s privacy and personal data, reflected in the EU’s GDPR-regulation. This reality will catalyse a European way for the development technologies against COVID19. The Belgian government, for instance, included its Data Protection Authority and an ethical committee in its Data Against Corona Taskforce, next to epidemiologists, telecom representatives, and data science experts.

The German government was not idle either and managed to organise a nation-wide #WirvsVirus. Being the biggest hackathon in Germany’s history, the event attracted over 40,000 participants who have put forwards thousands of different ideas. Interestingly enough, in the Czech Republic, a similar initiative has started, with nine leading IT companies joining forces to fight the pandemic, founding Covid19cz. The initiative attracted over 1300 volunteers, and the Czech government expressed enthusiasm to provide any necessary support for further development of the programme.

Another very promising development is Pan-European Privacy-Preserving Proximity Tracing initiative. The initiative unites over 130 participating organisations from eight European countries, and developed new technology to trace human contacts with respect for one’s personal data and privacy, and in line with GDPR. The system logs contacts identified by measuring radio signals such as Bluetooth without recording personal information or geolocation of its users. The source code is now freely available to all other countries who would like to develop similar systems of their own.

Still, it is very important to keep in mind that smartphone penetration in some parts of Europe is lower than in many Asian countries. Moreover, the use of smart devices is especially low for the most vulnerable population of seniors. Yet another problem is the combination of data from various sources which are often based on different technologies such as location data or communication data etc. This is especially true with the existence of multiple individual solutions without a central authority to coordinate and combine them. Lastly, the potential for privacy infringement through the increased use of location-based services might cast doubts on the necessity of such applications and reduce buy-in from citizens.

The European GNSS Agency (GSA) launched a great initiative, creating a useful repository with various developed applications against COVID19 during this difficult period. The potential use-cases are vast, and the current range already includes things like queue management, virus spread tracking, and response management. We absolutely recommend you to have a look!

Stay home, stay safe!

At the end of the day, it is essential to remember that any technology is just a mere tool in our hands and not an ultimate remedy. It is up to every single one of us to be highly conscious of the situation. GNSS.asia wishes all its readers good health, and for those impacted, a good recovery. Stay home, stay safe and take care of yourselves and your beloved ones!